The path to achieving Australia’s net-zero targets will take time and require substantial market support. The opportunity for Australian banks to fund renewable projects as part of Australia’s commitment is enormous and will not only help the government meet its emissions targets but drive growth.

The Paris Agreement and COP 26

The Paris Agreement’s aim is to strengthen the global response to the threat of climate change and limit the increase in global temperatures to below 2°C above pre-industrial levels.

The Paris Agreement entered into force on 4 November 2016 after at least 55 parties (countries) that make up at least 55% of global emissions ratified the agreement. After the initial threshold was reached, 196 countries, including China, India, the European Union, and New Zealand have ratified the agreement. The USA initially was part of the agreement but notified the UN that they would withdraw from it as soon as it was eligible to do so – effectively Nov 2020. US President Biden has indicated that they will reenter the agreement.

The Intergovernmental Panel on Climate Change (IPCC) suggests that global warming above 2°C would have serious consequences, including an increase in the number of extreme weather events.

In the lead-up to the Paris Conference of Parties (COP), countries submitted Intended Nationally Determined Contributions (INDC) that set out each party’s plans for addressing climate change, including a target for reducing greenhouse gas (GHG) emissions, and how those targets would be achieved.

Assessing the outcome for the recent COP26 in Glasgow is difficult. Climate Action Tracker believes that only the EU, UK, Chile, and Costa Rica have adequately designed net-zero targets. However, the net-zero commitments now cover some 80% of total emissions and the 1.5°C ceiling is a clear consensus. The private sector commitments were arguably the biggest surprise, differentiating it from previous COP meetings.

The sectorial commitments on ending coal-fired power, global methane pledge, road transport, and deforestation were all extremely positive and tangible developments. However, China, India and Russia are notable omissions from most new initiatives which will dilute the impact.

The number of countries committing to net zero has now increased substantially, though many commentators point out that the implementation plans are weak.

However, over 140 countries covering some ~90% of global emissions have announced – or are considering – net-zero targets (not all by 2050). This is an increase from 130 countries covering ~70% of global emissions as of May 2021.

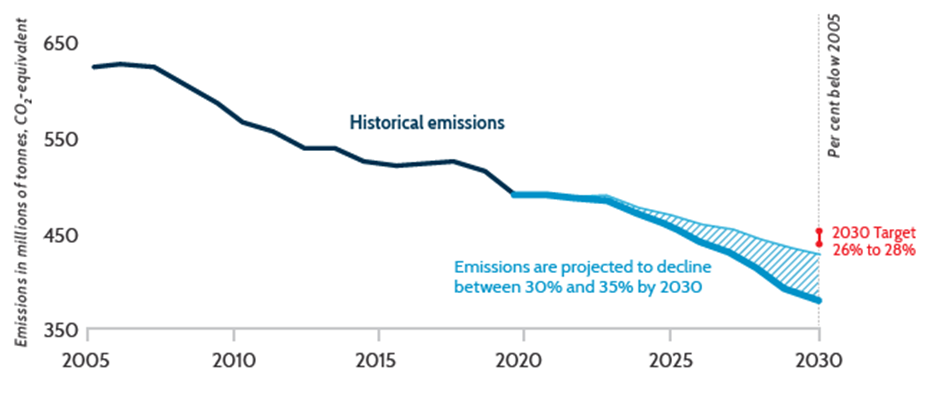

Pleasingly, Australia is on track to beat its 2030 emissions target (down 35%). Since 2005, emissions have reduced by over 20% in an economy that is now 45% larger (Chart 1). Australia went into COP26 with a new net-zero plan by 2050 that consists of reductions to date (-20%), technology (-40%), global technology trends (-15%), international and domestic offsets (-10 to -20%), and further technology breakthroughs (-15%). The technology-heavy, detail-light promise has plenty of critics.

Chart 1. Australia’s carbon emissions 2030 target

Source: Australian Government

Bank funding of fossil fuels

As part of their commitment to reduce Scope 1, 2 & 3 GHG emissions, all four major Australian banks are reducing their exposure to funding of fossil fuel companies. The disclosures are all slightly different but essentially aim to reduce and finally eliminate all funding of thermal coal mining and coal-fired power generation.

Part of the process is to engage with customers to help reduce the exposure and to provide a pathway to transition away.

ANZ

ANZ is targeting a 24% reduction of scope 1 & 2 emissions by 2025 and 35% by 2030 against a 2015 baseline. ANZ has substantially outperformed its targets, with scope 1 & 2 emissions reduced by 47% since 2015.

ANZ supports the Paris agreement goal of transitioning to net zero emissions by 2050. The company has several priority areas including:

- Engaging with 100 of their largest emitting business customers to support and establish or strengthen transition plans. These customers produce around 30% of the national total for Australia.

- Continuing to reduce the carbon intensity of their electricity generation portfolio by only directly funding low carbon gas and renewable projects by 2030. Renewable generation assets make up 88% of their electricity generation assets, and ANZ is committed to reducing the emissions intensity of its power generation portfolio by 50% on 2020 levels by 2030.

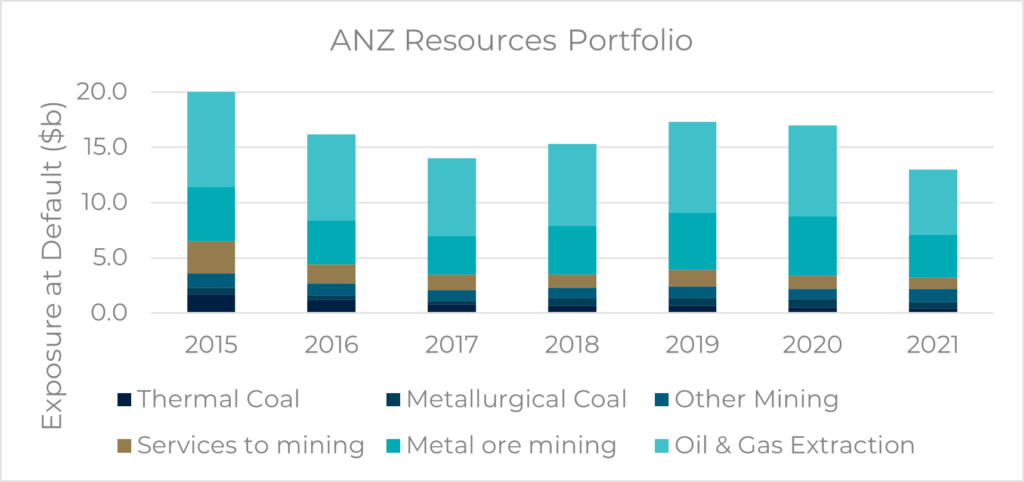

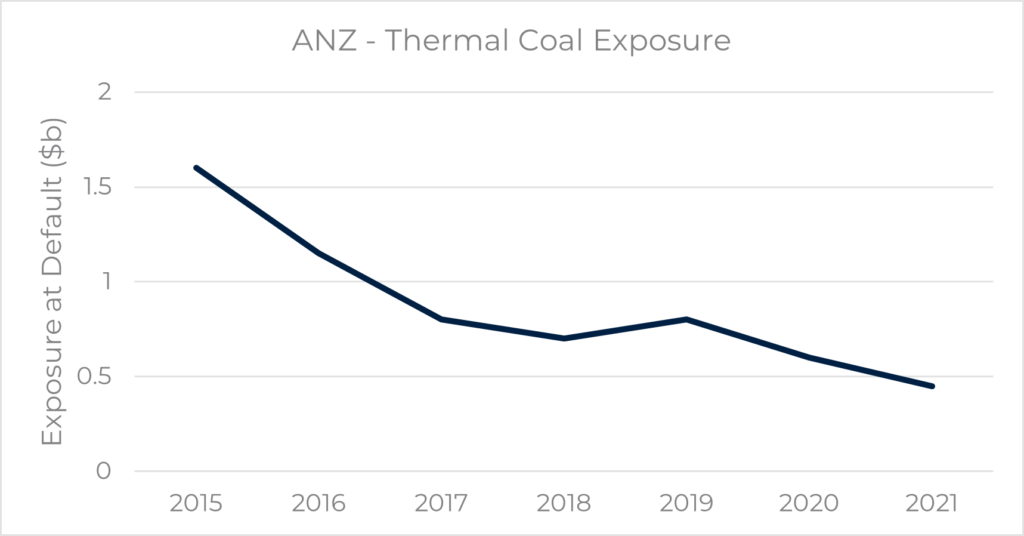

- Not directly financing any new coal-fired power plants or thermal coal mines, including expansions. The existing direct lending will run off by 2030. Thermal coal exposure has reduced by 75% since 2015 (Chart 3) and direct exposure to renewables has increased by ~55%.

- Targeting funding and facilitating at least $50b towards sustainable solutions for customers by 2050. The bank has funded and facilitated ~$2b towards this target since Oct’19.

- Financing only new large-scale office buildings that are highly energy efficient. ANZ are also committed to reducing the emissions intensity of its Australian large-scale commercial real estate portfolio by 60% on 2019 levels by 2030.

- Accelerating their own emissions reductions, with scope 1 & 2 emissions decreasing by 47% and tracking ahead of their 2025 and 2030 targets.

- By sourcing 100% of electricity from renewables by 2025.

Chart 2. ANZ Resources Portfolio

Source: Australia and New Zealand Banking Group Limited

Chart 3. ANZ Thermal Coal Exposure

Source: Australia and New Zealand Banking Group Limited

CBA

CBA is committed to the Paris agreement and is supporting the transition to net zero emissions by 2050. Its commitments include:

- Reaching 100% of their electricity needs from renewable sources by 2030. CBA is committed to setting science-based emissions reduction targets for scope 1 & 2, as well as scope 3 emissions. CBA has reduced scope 1 & 2 emissions by 40% since 2014.

- Continuing to reduce exposures to thermal coal-fired power stations and thermal coal mines to exit the sector by 2030.

- Provisioning of banking and financing to new oil, gas, or metallurgical coal projects if supported by an assessment of the environmental, social, and economic impacts and if in line with the goals of the Paris Agreement.

- Setting a target in 2017 of making $15b of funding available by 2025 to projects with a Low Carbon footprint. Eligible projects include renewable energy, 6-star rated green buildings, energy efficacy projects, and low carbon transport. This target has now been replaced with a sustainability funding target of $70b in cumulative finance by 2030.

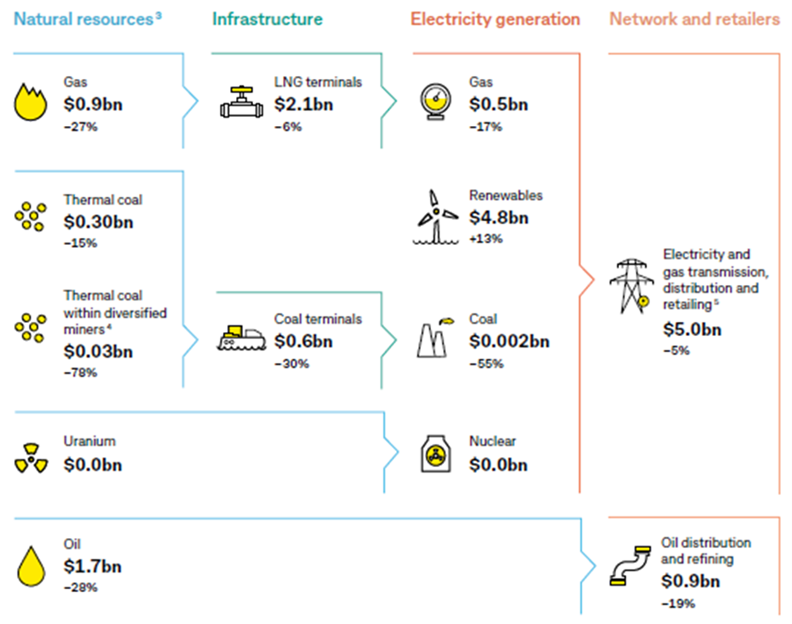

Chart 4. CBA’s Energy value change exposures as at 30 June 2021 (changes are since FY20)

Source: Commonwealth Bank of Australia

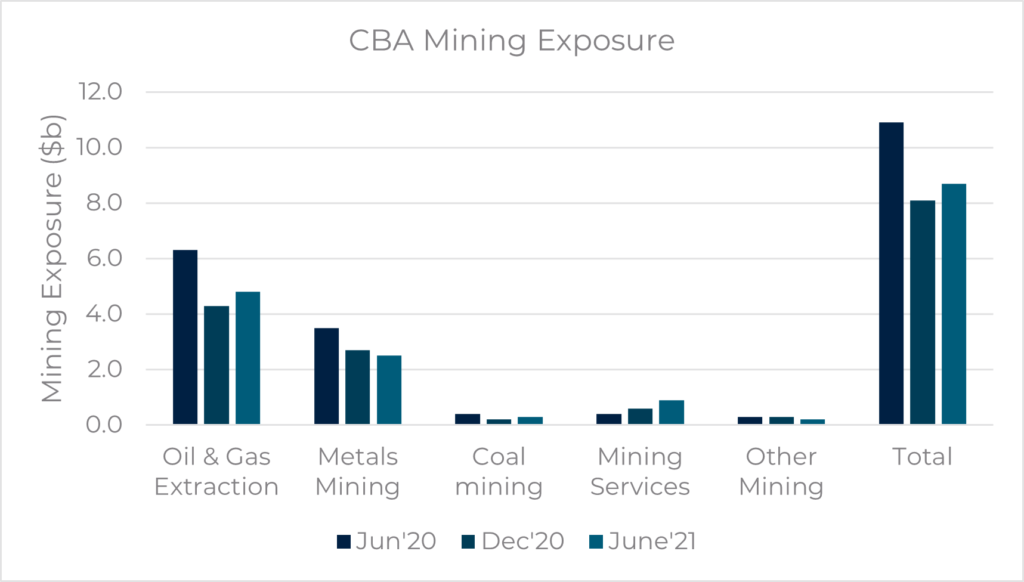

Chart 5. CBA’s Total Committed Exposure in Mining

Source: Commonwealth Bank of Australia

NAB

NAB will source 100% of their energy requirements from renewable sources by 2025 and has been carbon neutral in operations for over a decade. A science-based target to reduce GHG emissions by 51% by 2025. NAB has been committed to the Task Force on Climate-Related Financial Disclosures (TCFD) since 2017. Its commitments include:

- Being one of 36 banks globally to sign the Collective Commitment to Climate Action (CCCA). The CCCA is an independent initiative of the Principles for Responsible Banking (PRB) that sets out concrete and time-bound actions required for banks to align their lending with the objectives of the Paris Agreement.

- Working towards achieving a lending portfolio that is aligned with Paris Agreement net-zero emissions by 2050, including an environmental financing target of $70b by 2025 ($42.5b currently).

- Completing a risk review of the oil and gas sector using the IEA’s net-zero emissions scenario as a key reference point to guide NAB’s decarbonization pathway. Oil and gas only represent 0.3% of the NAB’s exposure at default (EAD).

- Capping oil and gas exposure at default at US$2.4b and reducing their exposure from 2026 through to 2050, aligned to IEA NZE 2050.

- Capping thermal coal mining exposures at Sept ’19 levels with a 50% reduction of coal mining financing by 2026 (was 2028) and therefore effectively zero by 2030 (previously 2035). NAB will not finance new thermal coal mines or coal-fired power facilities. Renewables now comprise 71.4% as at Sept ’21 of energy generation EAD, having increased from 39% in Sept’14 (Chart 6).

- Working closely with its 100 largest GHG emitting customers to support them in developing and/or improving low carbon transition plans by 2023.

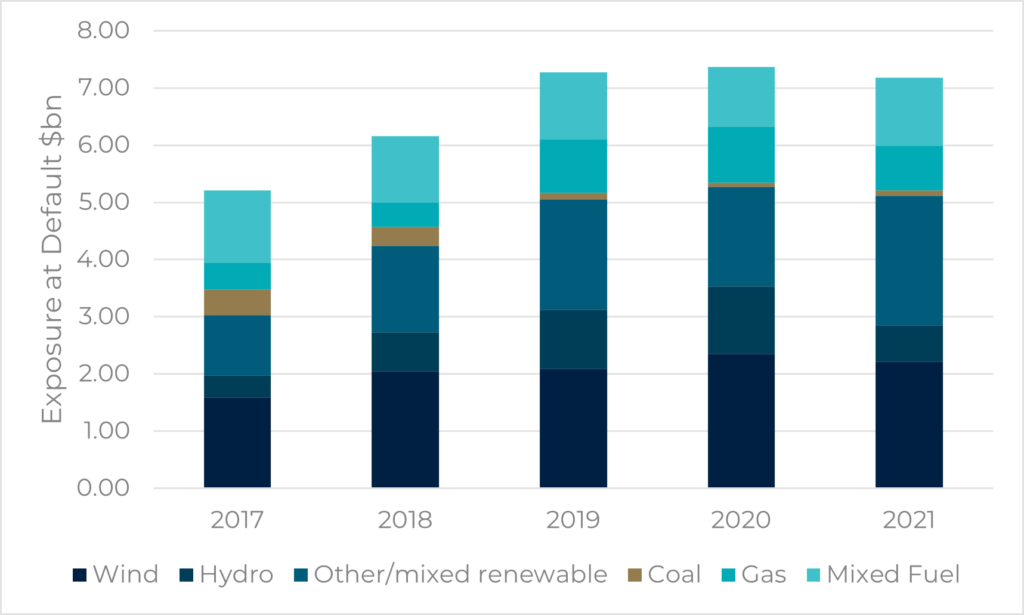

Chart 6. NAB’s Power Generation exposures measured by total Exposure at Default ($bn)

Source: National Australia Bank

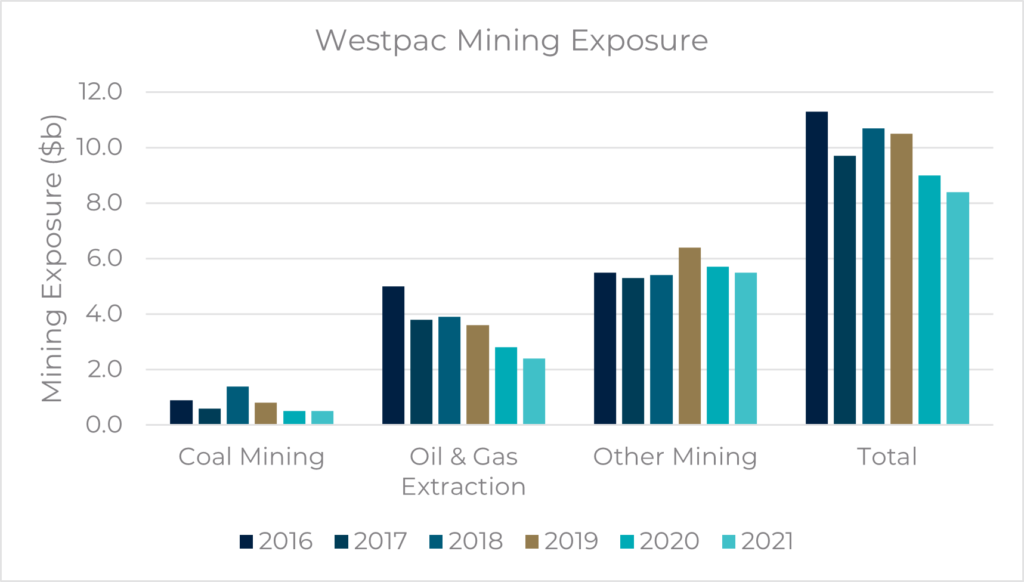

Westpac

Westpac is committed to managing the business in alignment with the Paris agreement and the subsequent net-zero transition by 2050. The bank is working to:

- Source the equivalent of 100% of their global electricity consumption through renewable sources by 2025. Scope 1 & 2 emissions are down 58% from the 2016 base year and thus on target for the 85% reduction by 2025 and 90% by 2030.

- Continue to reduce scope 3 supply chain emissions, which are already down 20% from the 2016 base year and compare favourably to the 35% reduction target by 2030.

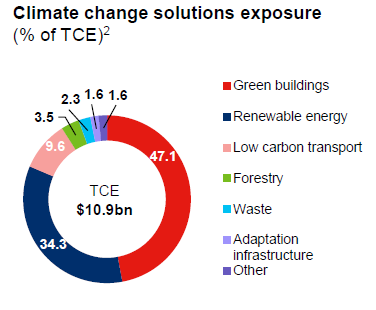

- Provide $3.5b of new lending to climate change solutions by 2023 and $15b by 2030 with $1.9b in new lending so far.

- Reduce Scope 1 & 2 emissions by 85% by 2025 and 90% by 2030 using 2016 as a base year. In addition, Westpac is working to reduce Scope 3 supply chain emissions by 35% by 2030.

- Ensure no new thermal coal customers, leading to no exposure by 2030.

- Support greenfield renewable projects in Australia, with 24 added since 2016 that power ~2.7m households. The bank has also financed eight greenfield renewable projects that will power 800,000 homes.

- Provide new lending for oil and gas extraction, refining, and exploration to only those companies that publicly disclose Paris-aligned goals.

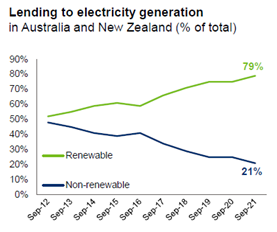

Chart 7. Westpac’s electricity generation lending over time & Climate change solutions exposure

Source: Westpac Group

Chart 8. Rising annual mean temperature in Australia 1910-2020

Source: Westpac Group

Cost of capital set to increase

The implication of banks ceasing, reducing, and phasing out funding thermal coal and fossil fuel projects is that the cost of capital increases. Many super funds within Australia and globally are either reducing or not investing in thermal coal exposed stocks, meaning the availability of equity is also reducing and/or becoming more expensive. Alternate sources of funding outside of Australia and private investment may become the norm.

Recent M&A in the oil and gas sector in Australia has been at least partly driven by these forces. The Oil Search/Santos merger increases the size of the company and therefore allows the business to rely less on debt and equity to fund projects. The BHP oil/Woodside merger is based around a decision by BHP to exit the oil and gas business as it has with thermal coal. The size and free cash flows generated by the merged business allow the company to rely less on external funding for new projects.

The listed thermal coal industry within Australia is small at around $5.b, with only Whitehaven, Newhope, and Washington H Soul Pattinson. South 32 has now exited its significant position in thermal coal assets in South Africa to Seriti Resources. Rio Tinto exited their longstanding exposure to thermal coal, and BHP is on a quick path to exit with recent sales of its thermal coal mines.

Funding of the transportation infrastructure for thermal coal is now also at risk. In our view, companies such as Aurizon Holdings that own and operate coal haulage operations in both Queensland and New South Wales are likely to have availability of funding reduced, and they are also likely to find asset owners excluding them from their investable universe. Dalrymple Bay Coal Terminal is another infrastructure asset that is at risk. Tyndall AM ensures that the life of coal assets and coal-related assets in our valuations expire well before 2050 in line with the Paris Agreement net-zero emissions target.

Tyndall AM has previously written about the impact of stranded assets in the context of coal-fired power stations. Our assessment was that it was immaterial for Origin Energy (c2%) and modest for AGL (5–10%). The potential funding of any new coal-fired power stations within Australia is highly unlikely post COP 26. No current power generator is discussing building new coal-fired power stations as they are focused on transitioning to renewables, with gas-fired power stations acting as firming capacity.

The Australian Energy Market Operator (AEMO) now expects coal fired plants to close at triple the pace of previous estimates. Victoria’s brown coal plants are now expected to be closed in just over a decade and the grid will be coal-free by 2043.

Post the nuclear submarine agreement with the USA and UK, nuclear as a power source is starting to be discussed although regulatory change is required.

The opportunity set for the banks to fund renewable projects is enormous as governments worldwide encourage and incentivise projects. Capital expenditure in global energy investments over the next 30 years (vs pcp) including the decline in fossil fuels is some 4x higher according to UBS Global Research. The current exposure that Australian banks have to coal, and coal-fired power stations is small, and, in all cases, the renewable exposure is greater and growing quickly. In total, the banks fossil fuel financing is approximately 0.8-2.5% of total lending. The banks have committed to ~$215b of sustainable financing targets by 2030 and since 2015 some $86b has been deployed. All the banks recognise that funding new renewable projects and supporting customers’ transition to net-zero emissions is the pathway to future growth. The Australian government’s pathway to net-zero is very technology-heavy and will require substantial support from the banks.