Iron ore prices may have finally found some stability moving forward

Recently, the People’s Bank of China (PBOC) rolled out its most significant set of monetary easing policies since 2015. These measures were designed to address China’s ongoing property sector challenges and provide a broader boost to economic growth. Interest rates and reserve requirement ratios have been cut to historically low levels, signalling the government’s commitment to maintaining liquidity and preventing a deeper slowdown.

While this has spurred a rally in both Chinese equities and Australian resource stocks, the question remains: Is this a short-term sentiment-driven bounce, or the start of something more sustainable?

While opinions may vary on the longevity of this rally, one thing is clear: China’s looser monetary policy has created an environment ripe for further fiscal and property policy adjustments. The current positioning of the market is quite negative on China and thus underweight stocks that are exposed to China such as Australian Resources. This helps explain the recent strong market reaction.

Have iron ore stocks found their floor?

The common reaction to China’s slowdown often involves calls to sell big miners like BHP (ASX: BHP) and Rio Tinto (ASX: RIO). However, that kind of knee-jerk reaction doesn’t align with a value-based investing approach. While sentiment undeniably influences short-term market movements, the real question is: How much steel is the global economy demanding, and what is the marginal cost of supply?

At current prices, iron ore is likely sitting at a support level, hovering around US$95/t, which is underpinned by break-even costs. Prices have dipped below US$95/t for only 16 days this year, compared to 50 days over the last three years. The cost curve supports this level, as many producers would be unprofitable at lower prices. Additionally, trader mentality tends to kick in once prices break the US$100/t threshold, adding further support to this range.

On a more fundamental level, we believe there is currently around 120mt of supply in the market that requires a price of over

US$90/t to stay profitable.

So, the question we have to ask is whether China’s economic weakness is severe enough to remove another 120Mt of iron ore demand from the market. We don’t think so.

While the Chinese government has signalled its willingness to address demand concerns through coordinated policies, the China Iron & Steel Association (CISA) has projected that crude steel production will remain flat year-on-year in 2024. This suggests stability moving forward at current levels.

Supply-side adjustments: Rebalancing the market

On the supply side, significant cuts in iron ore production from both India and China have already done much to rebalance the market. India’s output has fallen from 70Mtpa earlier this year to 30Mtpa due to price sensitivity, while China’s domestic production has similarly dropped from 200mtpa to 80mtpa on a 62% Fe basis.

In Australia, we have seen Mineral Resources (ASX: MIN) shut down the Yilgarn operations (8Mt) and the Sino Iron Project decreased from 21Mt to 14mt. These adjustments further underscore the market’s price elasticity.

The greatest long-term supply risk remains the Brazilian mining giant, Vale. Although Vale has increased its production guidance for the year, Brazilian exports typically flatten out in the final quarters of the year due to seasonality, so massive increases in output are unlikely.

Longer term, another potential supply-side disruptor that has long spooked the market is the Simandou project in Guinea. The rail line is expected to be operational by Q1 2026, with the port to be staged thereafter. The complexity of the project poses a significant risk of delays. We expect the operation to ramp up through 2028. Additionally, the wet season in Guinea introduces challenges with stockpile management and moisture control.

For now, the risk of an oversupply glut in the iron ore market seems overplayed by the bears in the market.

Seasonality and Sentiment

Another factor working in iron ore’s favour is seasonality. Historically, iron ore prices have shown strength from December through February, as China’s domestic production falls during the winter months. This forces the country to rely more on seaborne supply, which is often disrupted by wet weather conditions in Brazil and the Pilbara region in Australia.

Port inventories are currently sitting at 150Mt, which is on the higher end of the seasonal average. However, this doesn’t pose a significant threat to the market, as a portion of these inventories are now controlled by major iron ore players for blending purposes.

Moreover, low-grade discounts have narrowed, and rebar spreads have rebounded from their September lows, signalling that much of the bearish sentiment may already be priced in. It is also difficult to assess the full supply chain inventories in China including stockpiles at steel mills. Recent discussions with China companies suggest that this inventory may be at the lower end of history.

Where is the opportunity in iron ore equities?

In terms of equities, Fortescue Metals Group (ASX: FMG) is a recent addition to the portfolio. It offers an attractive entry point, and its lack of gearing makes it a pure play on a rebound in iron ore prices while paying an attractive fully franked distribution. BHP and Rio Tinto offer more diversified exposure, with their base metals businesses providing some downside protection.

While the market remains cautious due to weak Chinese sentiment, the fundamental factors supporting iron ore prices—cost support and seasonality—paint a more optimistic picture.

As long as demand holds and supply remains in check, iron ore prices are likely to stabilise around current levels, if not rise slightly through the remainder of the year. Given this, an overweight position in iron ore equities, particularly FMG, appears to be a solid investment in the months ahead.

Is this the start of a larger rotation out of the banks into the miners?

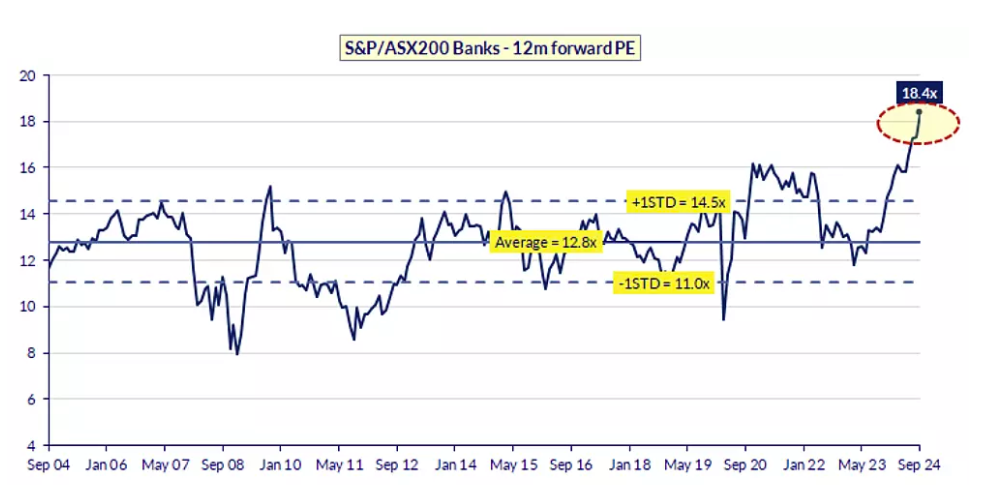

We are seeing a significant valuation gap between the Bank and Resource sectors. The Banks sector has surged to an all-time high P/E of 18.4x (refer to Figure 1), well above its historical average of 12.8x, even exceeding the +1 standard deviation level of 14.5x, indicating stretched valuations.

Figure 1: ASX200 Banks – trading at 18.4x forward concensus earnings (all-time high)

Source: Factset

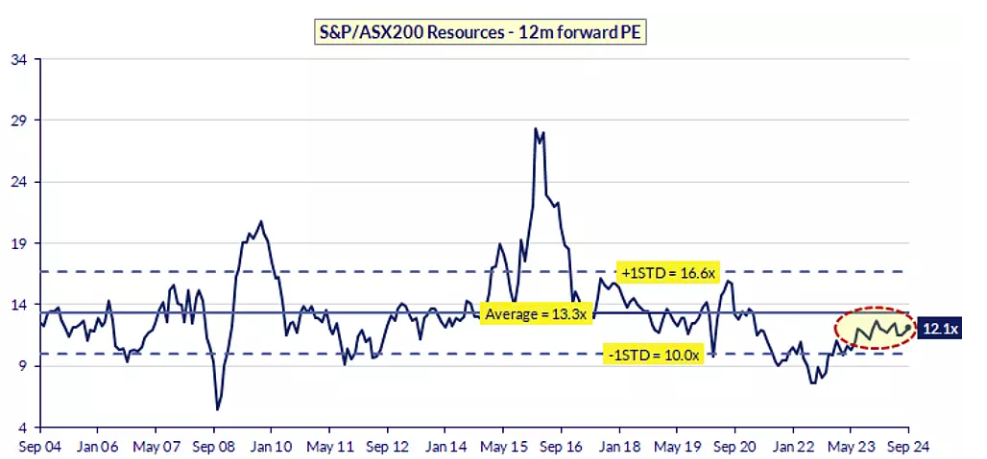

In contrast, the Resources sector is trading at 12.1x forward earnings (refer Figure 2), below its long-term average of 13.3x, making it the cheaper of the two sectors to own, which can be expressed through owning quality businesses like the iron ore majors. The stretched bank valuations have likely been partly an expression of the market being underweight China and resources given bank earnings have largely been in line with expectations.

Pristine asset quality and extremely low bad debts have been the prime drivers providing some modest earnings growth. The obvious catalyst for a bank correction was either via the resource’s rotation from confidence in a China recovery or the potential of a recession in either Australia or the USA. The former is emerging, and the latter is a realistic, albeit not a base-case scenario.